U.S. Cold Storage Market Distributor Analysis and Forecasts By 2030

U.S. Cold Storage Market Growth & Trends

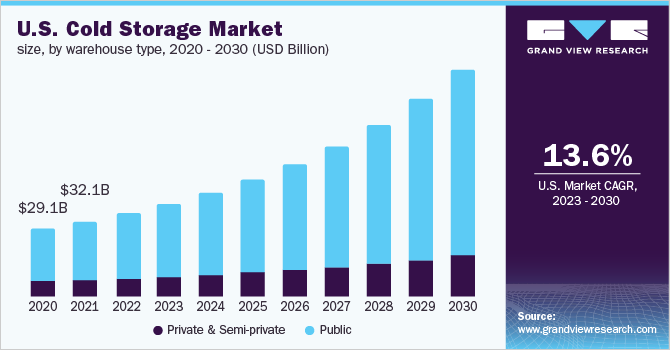

The U.S. cold storage market size is estimated to reach USD 96.90 billion by 2030, expanding at a CAGR of 13.6% over the forecast period, according to the new research conducted by Grand View Research, Inc. The U.S. is widely regarded as one of the leading markets in developing technologies responsible for the effective management of cold storage processes. The pharmaceutical industry is expected to offer growth opportunities to the market. Inventory management of pharmaceutical goods, such as vaccines and medicines, is an expensive process that necessitates adequate security measures to maintain product quality. Advanced cold storage technologies that offer beneficial features, such as advanced refrigeration technologies and monitoring and tracking systems of various products like fruits and vegetables, significantly mitigate the possibility of wastage of temperature-sensitive goods.

U.S. Cold Storage Market Segmentation

Grand View Research has segmented the U.S. cold storage market based on warehouse type, construction type, temperature type, application, and state:

Based on the Warehouse Type Insights, the market is segmented into Private & Semi-private and Public.

- In terms of revenue, the public segment dominated the market with a share of 78% in 2022, owing to its significant adoption among consumers on leased or short terms purposes at affordable costs. Based on the warehouse type, the market has been categorized into two segments, namely private & semi-private and public. A public warehouse is operated as an independent business or third-party provider that offers various services, such as handling, warehousing, and transportation for a fixed or variable fee. Public warehouses are also known as duty-paid warehouses that can be owned by an individual or some agency.

- Given the massive costs associated with the construction and maintenance of warehouses, only big companies can afford to own and maintain their private warehouses. However, the companies are increasingly constructing private warehouses as they offer significant benefits, such as flexibility, greater control over cost, and the ability to make decisions regarding the overall activities and priorities of the facility. Moreover, due to increased international trade and consumer spending, cold storage operating profits have risen dramatically in the last five years. Low-interest rates have also enabled operators to finance new constructions. The private and semi-private segment is expected to portray a significant CAGR of 11.1% from 2023 to 2030.

Based on the Construction Type Insights, the market is segmented into Bulk Storage, Production Stores, Ports.

- The production stores segment held the largest share in 2022 and is estimated to grow at the highest CAGR exceeding 15.6% from 2023 to 2030. This growth is attributed to the growing emphasis on the protection of goods, which include raw materials as well as finished food products throughout the production process in a plant. The bulk storage segment is also expected to proliferate over the forecast period. Bulk storage warehouses are suitable for storing fruits and vegetables in large volumes. They can also be used to extend the availability of other bulk materials such as flour, cooking ingredients, and canned goods while protecting them from spoilage and keeping them away from direct sunlight.

- Constructing refrigerated warehouses near ports can help simplify the customs procedures associated with the import and export of temperature-sensitive products. Improvements in efficiency and automation have widened the gap in operating performance between older and newer cold storage facilities. In the past few years, operators in the industry have implemented new technologies, such as high-speed doors, energy-efficient walls, automated cranes, and cascade refrigeration systems, to increase efficiency and reduce operating costs. For instance, the adoption of automated cranes has enabled operators to pile goods at greater heights, leading to an increase in the average building height of newer facilities.

Based on the Temperature Type Insights, the market is segmented into Chilled and Frozen.

- The frozen segment accounted for the largest share exceeding 81% in 2022. Increasing awareness about convenience food among individuals has led to a shift in their preference for ready-to-cook meals. Moreover, consumers are increasingly opting for frozen food owing to its support for microwave cooking and ease of use in terms of packing techniques. These trends have significantly contributed to the rise in the adoption of frozen foods, thereby leading to segment growth. However, the chilled segment is anticipated to witness a notable shift in growth over the forecast period.

- Based on temperature type, the market is segmented into chilled and frozen cold storage The warehouses falling under the chilled segment maintain their storage temperature in the ranges of above -5°C. They are used to store fresh fruits & vegetables, eggs, dry fruits, milk, and dehydrated foods, among others. Meanwhile, the warehouses falling under this segment maintain their temperature in the range from -10 to -20°F. They are used to store frozen vegetables, fish, meat, seafood, and other products.

Based on the Application Insights, the market is segmented into Fruits & Vegetables, Dairy, Fish, Meat & Seafood, Processed Food, Pharmaceuticals.

- The processed food segment is projected to witness highest growth of 16.9% from 2022 to 2030 owing to high demand of processed food products due to its several advantages such as immediate consumption, easy cooking, easy handling, and storage. Moreover, continuously changing lifestyle, increased safety, and growing need for easy convenience majorly drives the adoption of processed food. The adoption of processed food is also increased owing to excellent marketing and innovative packaging offered by the providers which further fuels the growth of the market.

- The increasing demand for perishable products and fast delivery requirements associated with the e-commerce-based food and beverage delivery market has led to a significant boost in cold chain operations. The processed food segment is expected to witness the highest CAGR over the forecast period owing to the continued improvements in food packaging materials. However, the growing incidence of food and pharmaceutical counterfeiting has resulted in the introduction of stringent government regulations regarding production and supply chains. These regulations are impelling industry incumbents to develop rigorous practices, and service providers are making investments in improving their infrastructure to obtain safety certifications.

Key Companies Profile & Market Share Insights

The key industry players engage in implementing several recent developments, such as setting up new facilities to offer avenues for increased profitability through improved customer relationships.

Some of the prominent players operating in the U.S. cold storage market include,

- Americold

- AGRO Merchants Group North America

- Burris Logistics

- Henningsen Cold Storage Co.

- Lineage Logistics Holdings, LLC

- Nordic Logistics

- Preferred Freezer Services

- VersaCold Logistics Services

- United States Cold Storage

- Wabash National Corporation

Order a free sample PDF of the U.S. Cold Storage Market Intelligence Study, published by Grand View Research.

Comments

Post a Comment